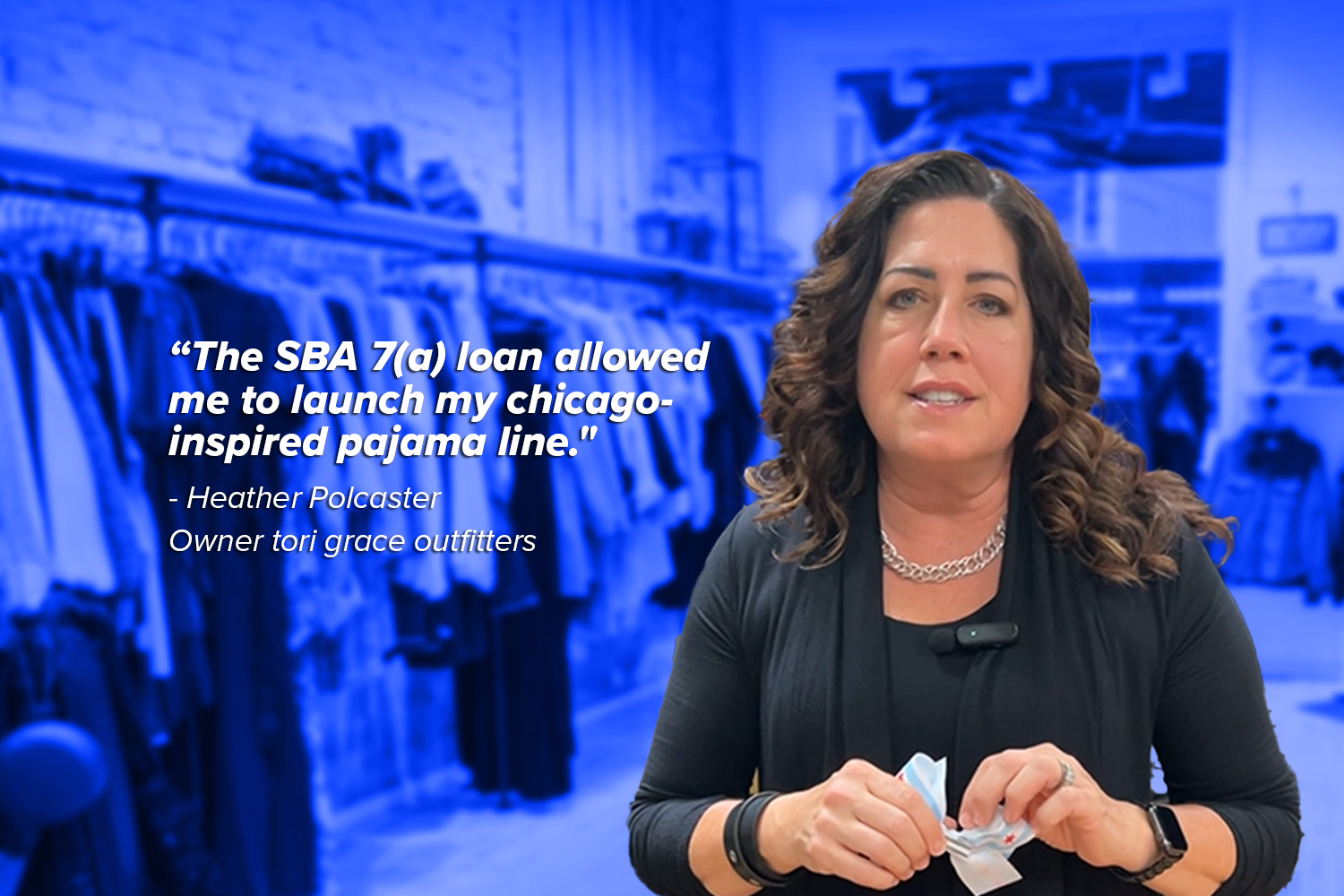

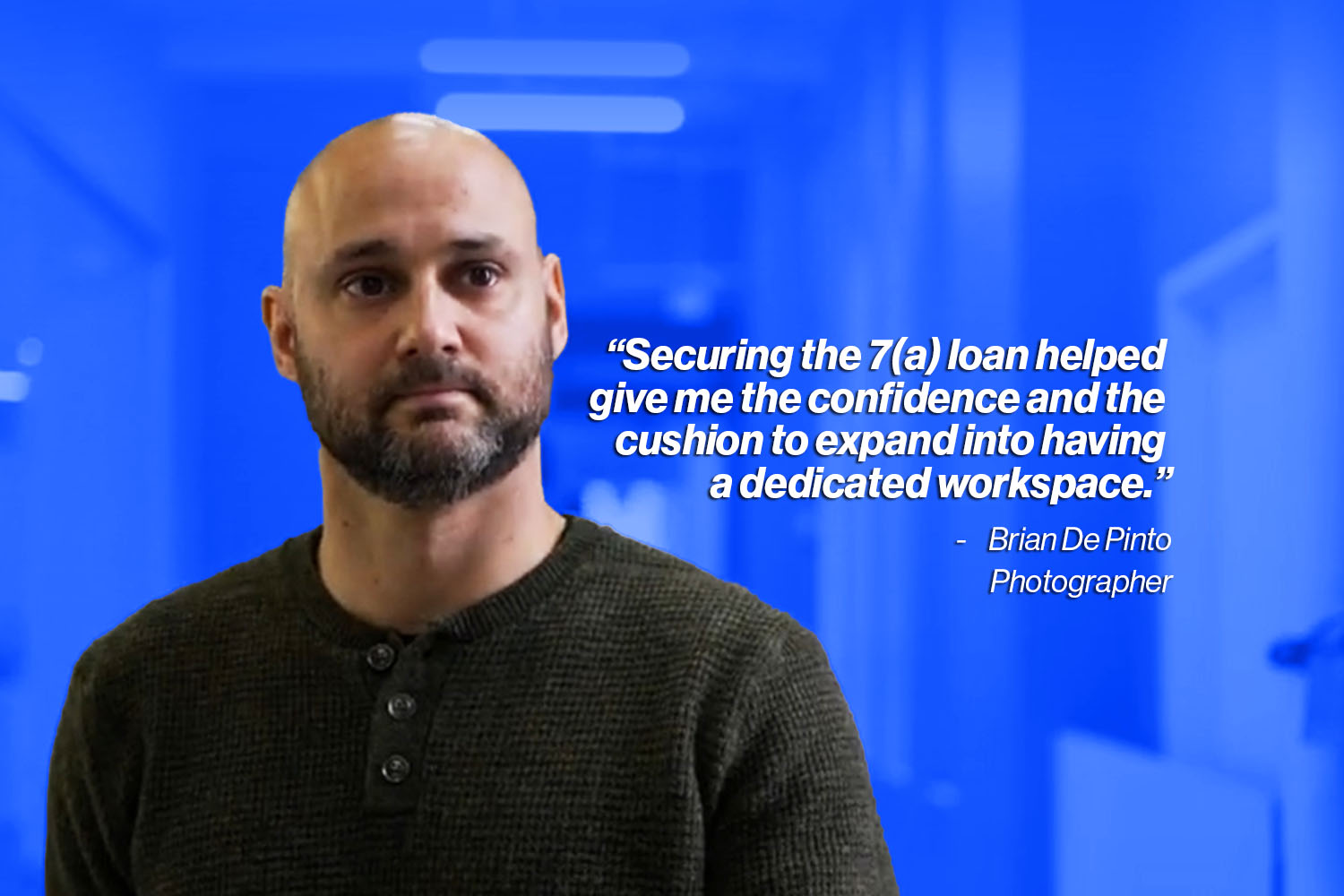

NEWITY is committed to helping small businesses across the United States thrive, which is why we offer SBA 7(a) working capital loans up to $500,000. Compared to alternative financing options, 7(a) loans offer lower interest rates and longer maturity that results in a lower monthly payment for your business.

To ensure a successful and seamless process for business owners, we’ve created a 3-part Insights series that include tips and tricks on how to prepare for your SBA 7(a) loan application:

- Part 1: Loan Eligibility – Explaining the main eligibility requirements for an SBA 7(a) loan.

- Part 2: Which Documents To Prepare and How – Outlining specific documentation necessary for the SBA 7(a) application and how to find and prepare each one.

- Part 3: SBA 7(a) FAQs on Applications – Answering specific frequently asked questions while applying for the SBA 7(a) loan. (Coming soon)

Required Documents for SBA 7(a) Loan Application

There are a number of documents business owners need to compile to begin their 7(a) loan application. However, we always remind our Members not to get overwhelmed, as you may have many of these documents on file. In the list below, we also included information on where to obtain each document if you don’t have it. For additional questions, reach out to NEWITY.

1. Entity Documents

- Articles of Organization or Incorporation – To verify the correct name and start date of the business, a filed copy of the articles and any amendments are required. You can obtain copies of these documents from your secretary of state using the list available here.

- Fictitious Name Filing – Also known as a DBA filing or Trade Name Certificate. This is required when your business operates using a name that differs from what is filed on your articles. You can file or obtain a copy of your existing filing using the list available here.

- Operating Agreement, Bylaws, Partnership or Trust Agreement – These documents specify the current ownership, rules, and regulations for managing the business. Although not required by all states, it is a best practice to have these prepared for your business. Check your state’s requires to verify these documents.

- EIN Confirmation Letter – Employers receive an EIN Confirmation Letter (called CP 575) to the address they provided on the SS-4 form, about 8-10 weeks after completing the Employer Identification Number (EIN) application on the IRS website and the issuance of their Federal Tax ID Number. A copy can be obtained by calling 1-800-829-4933.

2. Individual Documents

The following documents must be provided for all 20% or greater equity owners of the business:

- Personal Identification – Front and back image of valid and unexpired state driver’s license or state identification.

- Non-Citizen Identification – If a 20% or more owner is not a U.S. citizen, but is a lawful permanent resident, the following are required:

- Form I-9

- Copy of Permanent Resident Card (Front & Back)

- USCIS Verification & Authorization Letter

- Filed Tax Returns – The individual’s full unredacted tax returns for the three years preceding the loan request date.

- Personal Financial Statements – The SBA requires personal financial disclosures. To help with this, the NEWITY Smart Portal provides you with a template for completing your statements at the final stage before application submission. For an instructional video on how to complete the form, review our Personal Financial Statement resource.

3. Financial Documents

- Tax Returns – Full unredacted business tax returns for the borrower, guarantor, and affiliates for three years preceding loan request date (e.g. FY19, FY20, FY21). 2022 tax return required after April 18th, 2022 or copy of filed extension and proof of payment of estimated taxes. (Note: NEWITY requires up to the past three years of tax returns, however if your business is between 1-3 years in business, please submit the corresponding amount of documents.) Tax returns can include the following, depending on the business legal structure:

- Form 1040

- Schedule C or Schedule F

- Form 1065

- Form 1120 or Form 1120-S

- Balance Sheet – Your balance sheet must reflect financials within 90 days of loan request date. If you do not yet have a balance sheet, download a template and see our instructional video in the Balance Sheet Financial Template series.

- Year-to-Date Profit & Loss Statement – P&L with year-to-date totals through the reporting date, which must be within 90 days of the loan request date. If you do not yet have a P&L, download a template and see our instructional video in the P&L Financial Template series.

- Debt Schedule – This is a table listing your monthly debt payments in the order of maturity. Because this is a required document, we provide a fillable template in the application.

- Bank Statements – Operating account statements for the three months preceding the date of the loan request.

4. Miscellaneous Documents

- Copies of Franchise, License, Fuel Supply, Dealer or Other Third-Party Agreements – If applicable.

- Bankruptcy Explanation – A memo explaining bankruptcy filings, if applicable.

- IRS Payment Plans – Documentation regarding any existing IRS tax payment plans.

Where to Find More Information on 7(a) and Apply for your Loan

NEWITY offers small business 7(a) working capital loans up to $500,000. We’ve streamlined the SBA loan process for our members to make applying as simple as possible while standing by to guide you through every step. Start your 7(a) application here.

If you have questions about any of the required documents or where to find them, contact your NEWITY member services representative.

Looking for more information on 7(a) loans? Take a look through our other existing insights and stay tuned for the rest of our series on preparing for your SBA 7(a) loan application.