Economists predict The Federal Reserve will vote to maintain current interest rates next week, holding off on rate cuts until late 2024 if at all this calendar year.

Why isn’t the Federal Reserve adjusting interest rates?

While inflation crept to 3.4% in April, a stark improvement from 9.1% in June 2022, the current inflationary environment sits above the Fed’s 2% inflation target. Until inflation reaches 2%, it’s unlikely that interest rates will fall.

What does this mean for small businesses?

- Inflation appears to be tapering, even if ahead of Fed targets. While lowered cost of goods is not expected, 2022’s dramatic spikes of inflation appear to be in the past.

- Prolonged ‘high’ interest rates mean borrowing funds will continue to be expensive. Business owners holding out for a rate drop to secure a loan may be waiting beyond this calendar year before rates decline.

- Delaying loans for better rates isn’t a long-term solution. Businesses relying on credit cards will continue to pay interest rates near 21%, which is 86% more than an SBA loan.

Should businesses apply for a loan now?

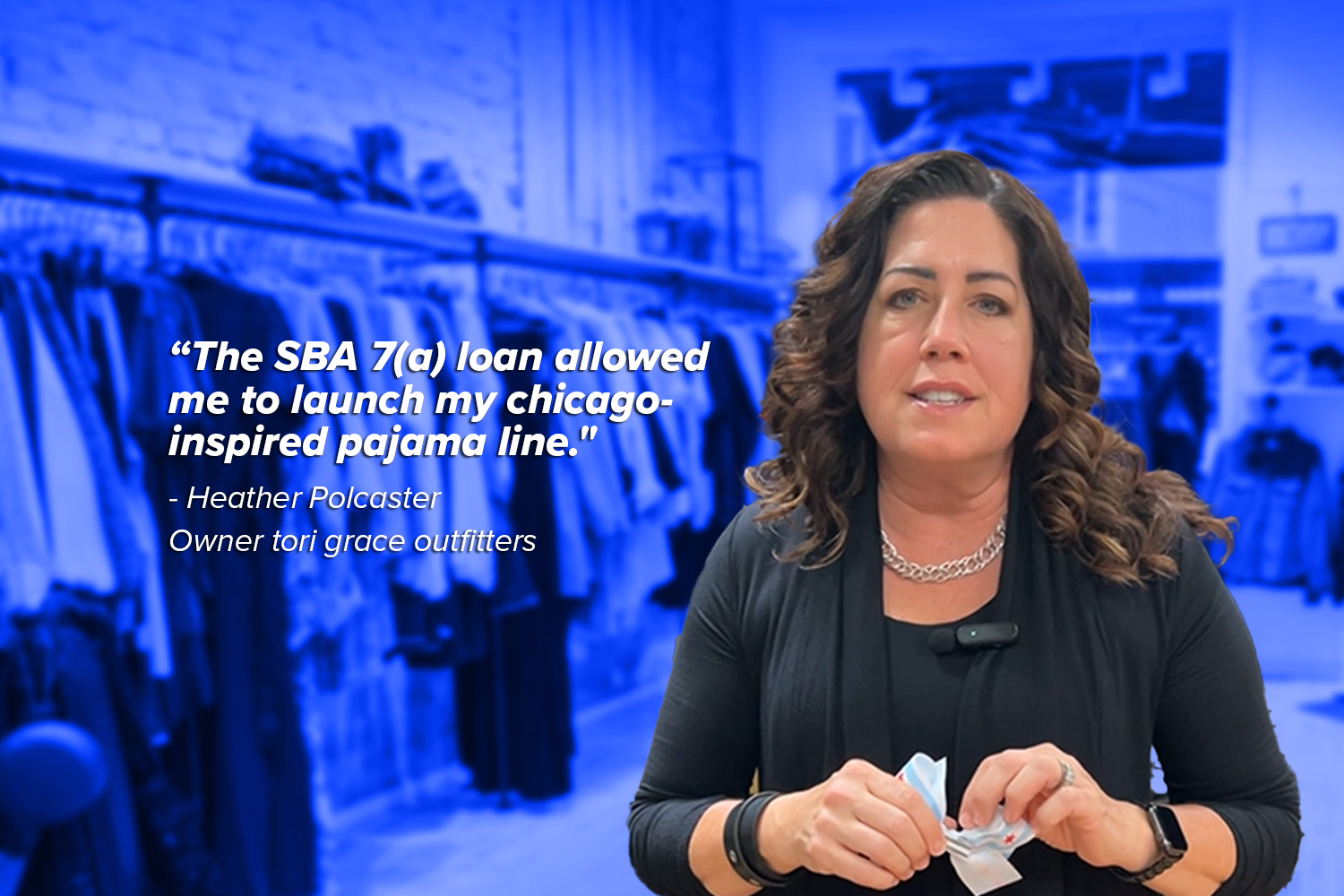

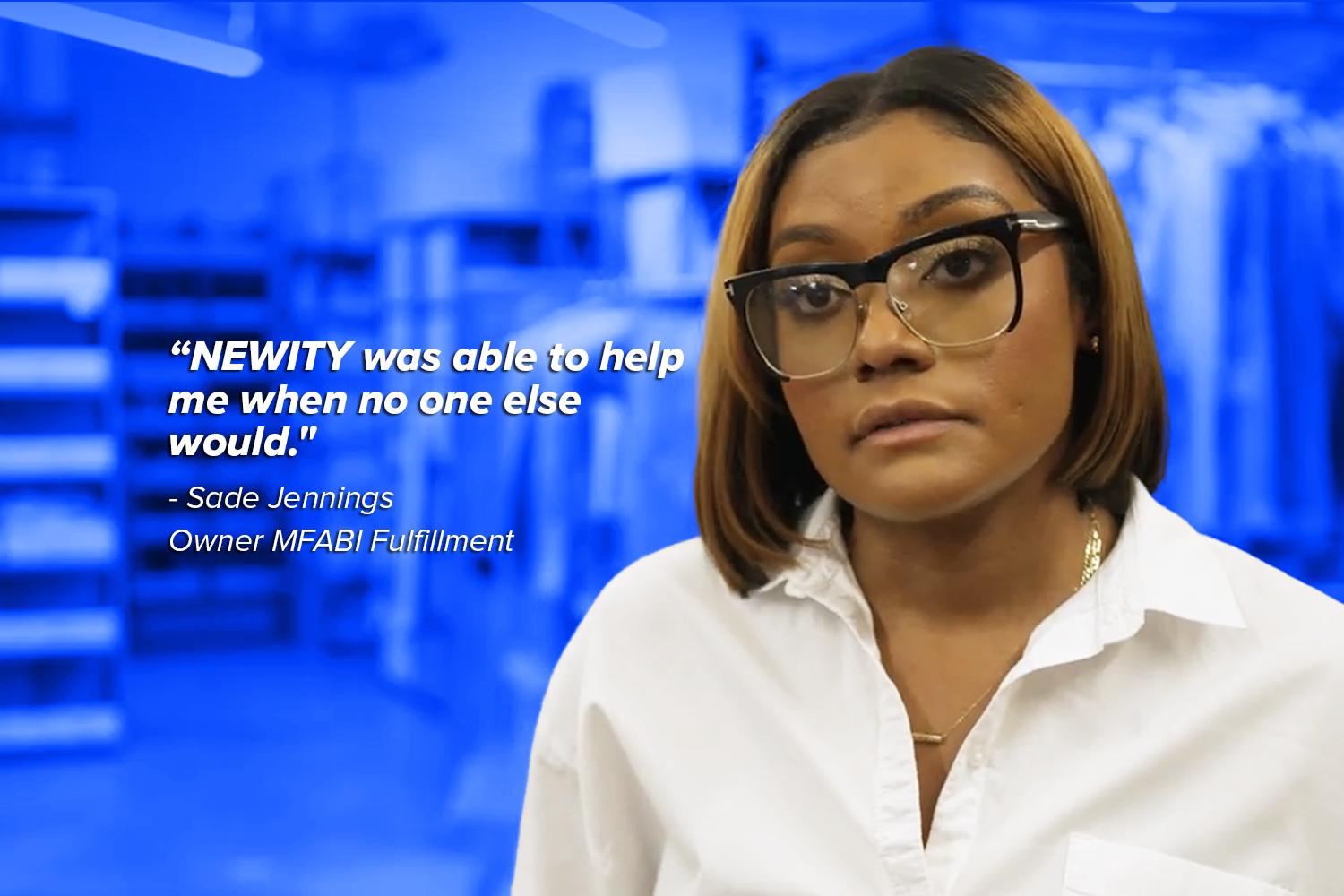

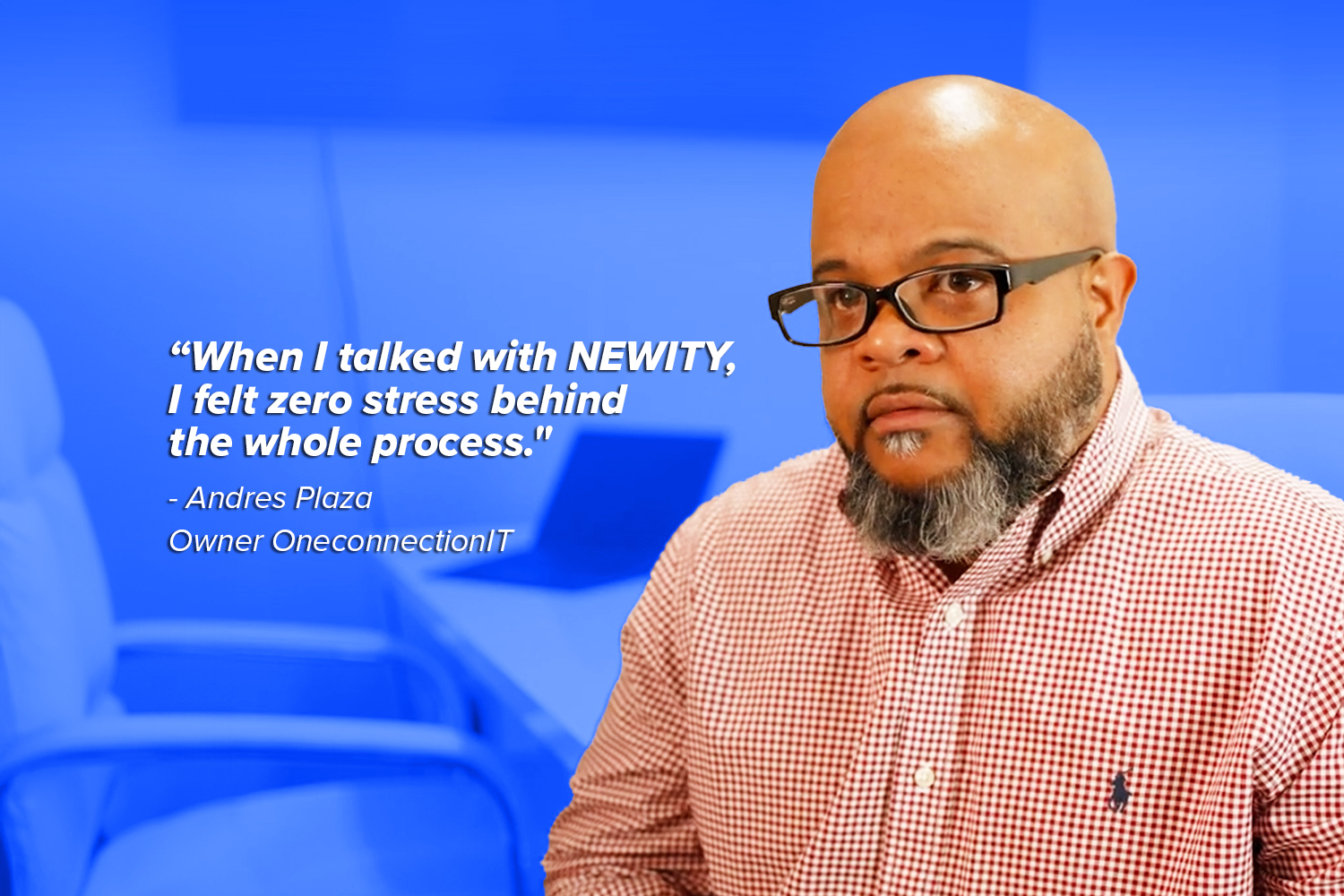

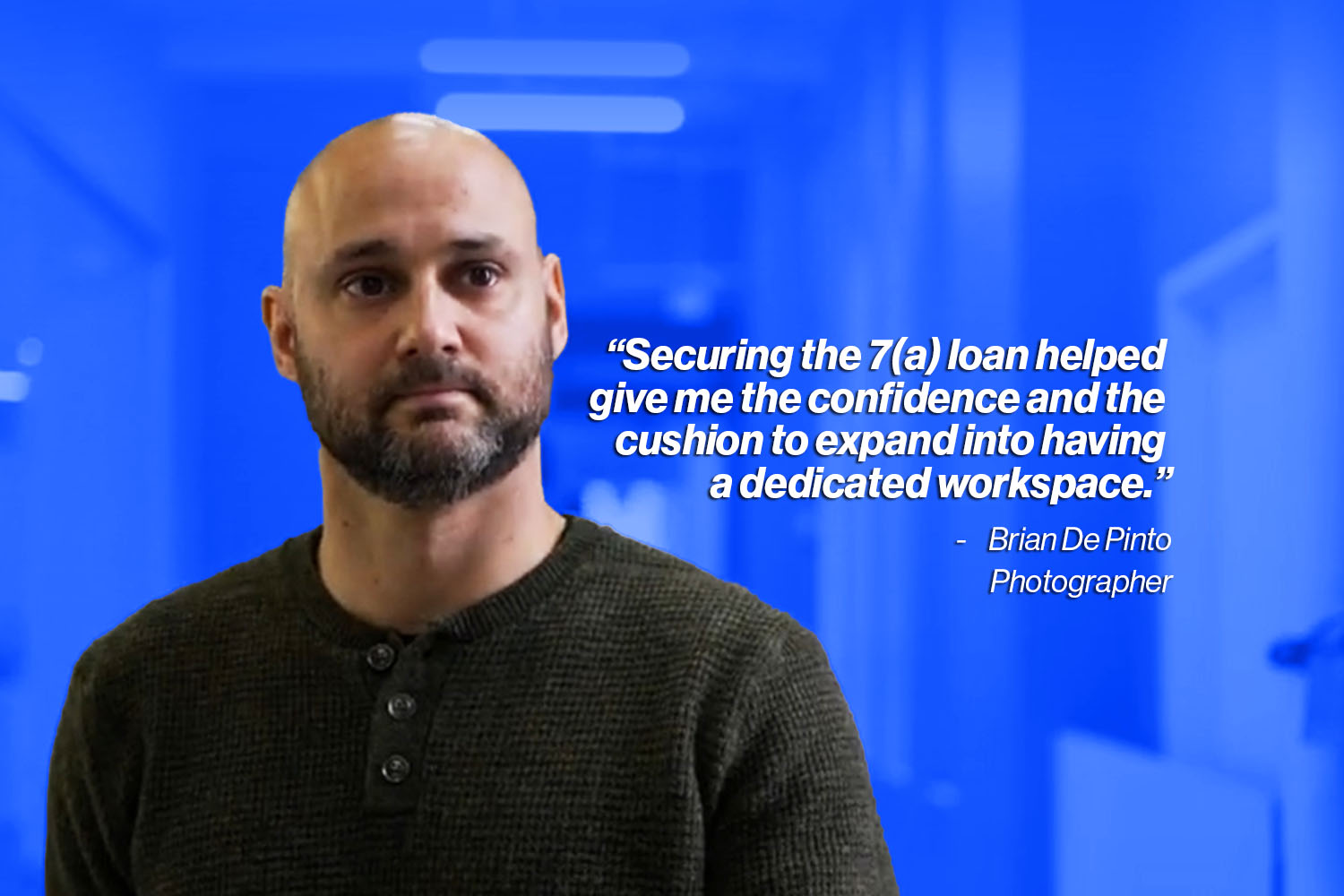

Yes, especially if you might qualify for an SBA loan. SBA loans offer some of the lowest interest rates over a 10-year period. As rates fall, businesses with SBA loans experience a reduction in payments throughout the remaining life of the loan. With no prepayment penalties, securing capital now allows you to deploy those funds without being locked into a high rate over a prolonged period.

If you’re not sure if you’re eligible for an SBA loan, we can help. You can determine if you qualify in less than 10 minutes without impacting your credit score.