What is a Statement of Cash Flows?

The Statement of Cash Flows – also known as the Cash Flow Statement – provides a detailed overview of a company’s cash inflows and outflows during a specified period of time (monthly, quarterly, or annually).

A Cash Flow Statement provides a picture of where the business stands on a cash basis by showing the funds that arrived in the company’s accounts. This is different from the income statement, which uses the accrual basis to show the income a business has generated or lost.

Why is the Statement of Cash Flows Important

Entrepreneurs can use this report to understand how much cash the company has on-hand to cover expenses and/or reinvest in the growth of the business (working capital). Any significant discrepancy between the statement of cash flows and the income statement could be indicative of operational problems such as unpaid accounts receivable (AR).

Additionally, the Cash Flow Statement can illustrate:

- The results of your cash planning

- How your money is being spent

- Ideas on how to increase cash inflows

- Cash stability in the event of a crisis

What Are the Sections of the Cash Flow Statement?

1) Operating activities

This section shows the inflow and outflow of cash from main operating activities, like selling or purchasing products and services. It reconciles a business’ net income to the actual cash received or spent by the company during these activities.

The cost and profit items included are also found on an Income Statement.

For example:

- Accounts receivable

- Accounts payable

- Inventory

- Wages payable

- Income taxes payable

2) Investing activities

This section focuses on the cash flows related to investment – a business’ purchase or sale of long-term assets like property, plant, and equipment (PP&E) or investment securities. The section also provides further detail on the assets owned by the company.

3) Financing activities

Finally, this section covers all cash flows relating to financial areas like long-term liability and stockholder equity accounts.

This can include:

- Notes payable

- Retained earnings

- Dividend payments

Financing activities will also show the company’s net cash flow, including things like the issuance of stocks or bonds and debt financing (e.g., bank loans).

How to Interpret a Statement of Cash Flows

A Cash Flow Statement provides a good indication of your company’s financial health and can shed light on how you can improve your cash position. Cash flow is typically seen as either positive or negative:

Positive cash flow

If the report shows positive cash flow, this indicates that the business is bringing in more money than it is spending during a specific time period. Having extra cash enables the company to use that cash to cover future expenses, reinvest in the business and its shareholders, pay off debt, etc.

It’s important to note, however, that positive cash flow does not definitively mean the business is profitable. These two things are not always correlated: you can be profitable without positive cash flow and you can have positive cash flow without earning a profit. Using an analysis of the Cash Flow Statement in conjunction with other Financial Statements will give a full financial picture of your business.

Negative cash flow

This is the less optimal situation, where your cash outflow (spending) is higher than your cash inflow (earning). As mentioned above, this doesn’t necessarily mean the business isn’t profitable, but likely means a deeper financial analysis may be necessary.

Negative cash flow over a specific period could mean you’re spending more than you’re making. It could also be a result of expansion or investment in long-term growth. This is why it’s helpful to look at changes in cash flow over time to understand performance.

Example in Practice: Statement of Cash Flows

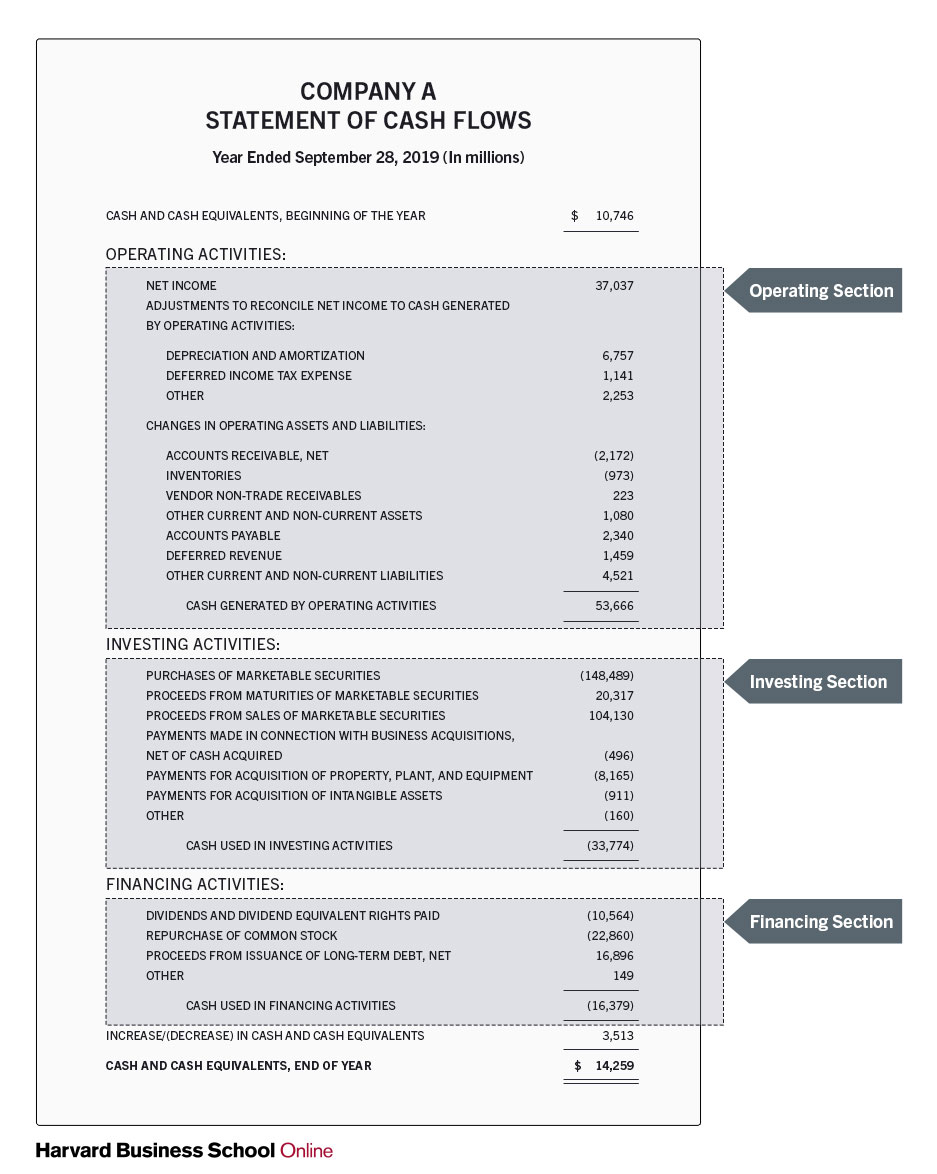

Here is an example of a statement of cash flows published by the Harvard Business Review:

As you can see, the statement includes the three sections – operating, investing, and financing – and gives a total “Cash and cash equivalents, end of year” of $14.259 billion (a positive cash flow). These numbers are likely much higher than a small business would deal with, but it’s a good example of the types of inflows and outflows often included in the statement.

It’s a lot of work to keep up with all the financial statements you need to run your business.

If you want help from experts you can count on, NEWITY partnered with Xendoo to take care of all your accounting needs in one place. With Xendoo, you get access to real people, real bookkeepers, and real CPAs who are ready to help you reach financial success.

Get Assistance with your Bookkeeping Today