How NEWITY Supports Its Members

Key Takeaways Whether you’re applying, uploading documents, or waiting on underwriting, our Member Services team is your go-to team for help, updates, and escalation. Our

How To File For Tariff Refunds

Key Takeaways The Supreme Court has ruled Trump’s IEEPA tariffs unlawful This ruling opens the door for many businesses to get refunded for IEEPA tariffs

How To Choose a Small Business Loan

Key Takeaways Small business loans through traditional banks have become less accessible and affordable Some financial institutions are introducing AI into their lending processes, making

AI In Lending— Is AI Deciding Who Gets Loans?

Key Takeaways Small businesses on average receive funding at less than half the rate of larger enterprises Traditional banks cannot justify the cost of funding

QBI Deductions— What Are They? Does Your Business Qualify?

Key Takeaways A QBI allows eligible businesses to deduct up to 20% of their business’s qualified income from their taxes, allowing them to secure a

2026 Small Business Taxes— Deadlines, Forms, and Extensions

Key Takeaways Ensure you know your EIN number and your business’s entity type in order to identify your payment and filing requirements This article lists

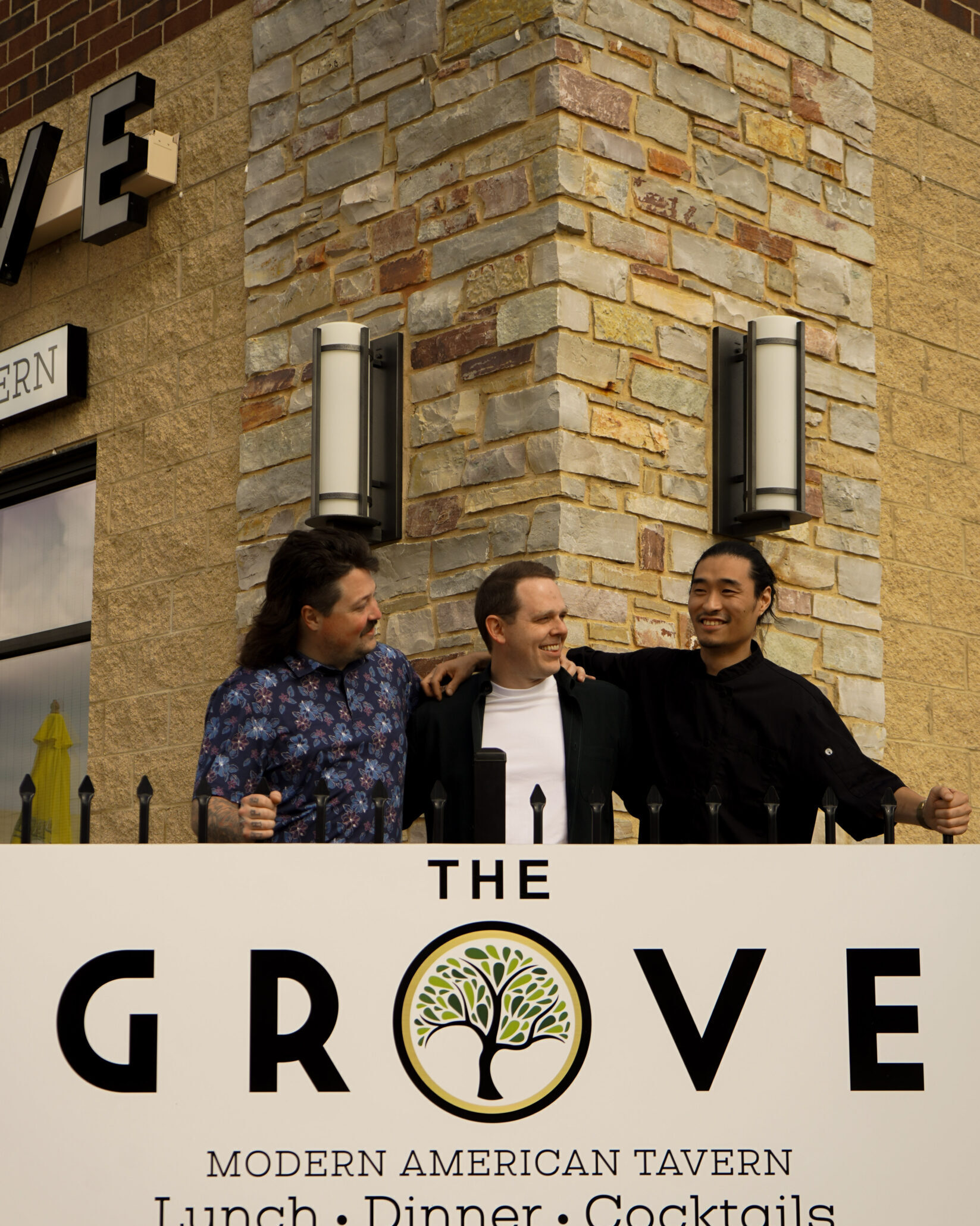

The Grove Tavern— Hometown Friends Turned Business Partners

Erected in the center of DeKalb, IL from nothing but a concrete slab stands The Grove Tavern. Owned by born-and-raised DeKalb natives, at the heart

NEWITY Wrapped: 2025 in Review

NEWITY’s 2025 Year Wrapped: A Year of Record-Breaking Growth and Impact As 2025 comes to a close, NEWITY is proud to reflect on a year

Managing Your Small Business Debt

Key Takeaways Start by organizing all your accounts, clearly indicating how much you owe, to whom, and by when. Consider various strategies to reduce your

Preparing Your Small Business For The Holiday Season

Key Takeaways Get festive with your online presence, sharing holiday-themed posts and drawing attention to your holiday season deals Consider expanding your hours to cater

Increase Your Small Business Loan Size

Key Takeaways Factors like your revenue, credit, debt, and business age all impact the funding you qualify for Paying down existing debt, opening credit building

4 Metrics To Track Your Business’s Financials

Key Takeaways Gross Margin shows how efficiently your business is producing and selling its products or services. Customer Concentration is a way to assess how

Small Business Bookkeeping

Key Takeaways Bookkeeping includes functions like transaction recording, account management, payroll processing, reporting, and more There are 5 account categories for sorting transactions: assets, liabilities,

Building Your Credit Score— Tools and Strategies

Key Takeaways Your personal credit plays a role in your business credit, so it’s best practice to focus on maintaining your finances in all areas

Can You Get an SBA 7(a) Loan If You Have Existing Debt?

Key Takeaways When you apply for an SBA 7(a) loan, the debt you already hold factors into how much capital you qualify for. You need

Government Shutdown: What it Means For SBA Borrowers

Key Takeaways A government shutdown occurs when congress cannot pass legislation for federal agency funding During this time, SBA loans cease being processed Submit your

Small Business Tax Planning

Key Takeaways Understanding the tax implications of your business’s structure can help you file properly and identify your tax advantages Consider opening an account on

What is an SBSS Score?

Key Takeaways Your SBSS score is your business’s credit score that accounts for several factors, spanning both business and personal finances SBSS scores range from

What You Can (And Cannot) Use an SBA 7(a) Loan For

Key Takeaways SBA 7(a) loans offer flexible funding for operational and growth needs. There are clear restrictions on how funds can be used, such as

Separating Personal and Business Finances

Key Takeaways Separating your business from your personal finances as much as possible will help you to stay organized, ensure your taxes are accurately filed,

Unsecured vs. Secured Credit Cards

Key Takeaways Secured credit cards require a cash deposit that acts as “collateral” on your card balance, and are easier to obtain for people with

Do You Need Collateral For An SBA 7(a) Loan?

Pledging collateral for a business loan can seem complicated, but it doesn’t have to be. In this article, we’ll break down the definition of collateral,

Your Business Loan Was Denied… What’s Next?

Key Takeaways SBA loan denial could be chalked up to poor credit, industry, or even business age You can reapply for an SBA 7(a) Loan

What is a NAICS code and why do they matter to my business?

Key Takeaways Your NAICS code helps you and others categorize your business at its most specific level NAICS codes are used for a variety of

How Business Owners Can Navigate Seasonal Slowdowns

Seasonal slowdowns are a reality for many businesses, whether you’re in retail, hospitality, or any industry affected by fluctuating consumer demand. While these quieter periods

Secured vs. Unsecured Loans

When small business owners look to borrow money, they often encounter two primary types of loans: secured and unsecured. Understanding the differences between these two

How To Effectively Repay Your Business Loan

Taking out a business loan can be a powerful tool for growth, whether you’re purchasing new equipment, expanding operations, or managing cash flow. However, repaying

How to Improve Cash Flow for Small Business Owners

Cash flow management is crucial for small business success. Positive cash flow ensures you can pay your employees, purchase inventory, invest in growth opportunities, and

How to Set SMART Goals for Your Small Business

Setting goals is essential for driving growth and success in your small business. But not all goals are created equal. To ensure your goals are

How to Plan for the Year Ahead: Start with a Strong Business Plan

As a small business owner, planning for the upcoming year is essential for sustained growth and success. A strong business plan serves as your roadmap.

Small Business Marketing ROI: Definition, Calculation, and Uses

No business owner wants to waste money on marketing tactics that don’t work. That’s why tracking and optimizing Marketing ROI is essential. It helps you

Scaling Your Small Business: How to Plan for Growth

Scaling a small business is an exciting milestone, but it comes with challenges that require careful planning. Scaling is different from simple growth. Simple growth

Top 6 Must Dos for Small Business Before the New Year

As December approaches, it’s the perfect time for small business owners to focus on 2025 planning. Setting yourself up for success starts with wrapping up

Business Term Loan vs. Line of Credit: What’s the Difference?

Term loans and lines of credit are two different ways small businesses can borrow capital from lenders. However, they operate differently and serve distinct purposes.

The Corporate Transparency Act and Beneficial Ownership Information Report: Everything You Need to Know

Small business owners need to stay informed about new regulations that may impact their operations. One such regulation is the Corporate Transparency Act (CTA), which

When Should I Get a Small Business Loan?

Access to capital is vital for small businesses, whether for growth, sustaining operations, or navigating challenges. However, deciding when to take on a business loan

Debt Consolidation vs. Refinancing

In the world of business finance, managing debt is a crucial aspect of keeping your operations running smoothly. Two common strategies for dealing with multiple

Business Loan Terms You Need To Know

You’ll encounter many terms when searching for a business loan. In this guide, we’ll walk you through all the essential terms related to small business

Small Business Loans for Women

Key Takeaways Women-owned businesses represented nearly half of all new startups in the U.S. as of 2024, up from 30% in 2019, totaling 12.3 million

Small Business Loans that Won’t Impact your Credit Score

As a small business owner, keeping track of your business’s financial health is crucial for long-term success. This includes monitoring cash flow, managing expenses, staying

Fixed vs. Variable Interest Loans: Which is Better for Your Business?

When it comes to financing your business, understanding the difference between fixed vs. variable interest rate loans is critical to making the best decision. Both

How to Apply for a SBA 7(a) Loan in 10 Minutes or Less

The SBA 7(a) loan program is a low interest, long-term, government backed loan for eligible small businesses. This program was designed for small businesses, so

How to Refinance Debt with an SBA 7(a) Loan

What is debt refinance? Debt refinancing replaces one or more existing debts with a new loan, often offering more favorable terms. This process helps businesses

Understanding and Managing Good vs. Bad Debt

Are you considering borrowing money? Many assume that all debt is bad, however, taking on debt for the right reasons can positively impact your financial

Debt Refinance; Boost your Business with an SBA 7(a) loan

Refinancing your debt can be a game-changer. If you’re carrying high interest debt, you’re not alone. Making high monthly payments can impair your cash flow

What are Startup Loans

Are you a small business owner seeking funding to grow your startup? You’ve probably encountered many ads for startup loans. Let’s explore what they are

Meet Sean and Helen – Pioneer Realty Group

“Being able to help our community, provide housing, and navigate the Real Estate landscape is our way of giving back to the community.” Sean and

ERC Update: Essential details from the IRS – June 2024

The IRS recently provided an Employee Retention Credit (ERC) update clarifying the status of outstanding claims, refund payment timing, and the processing moratorium. We’ve condensed

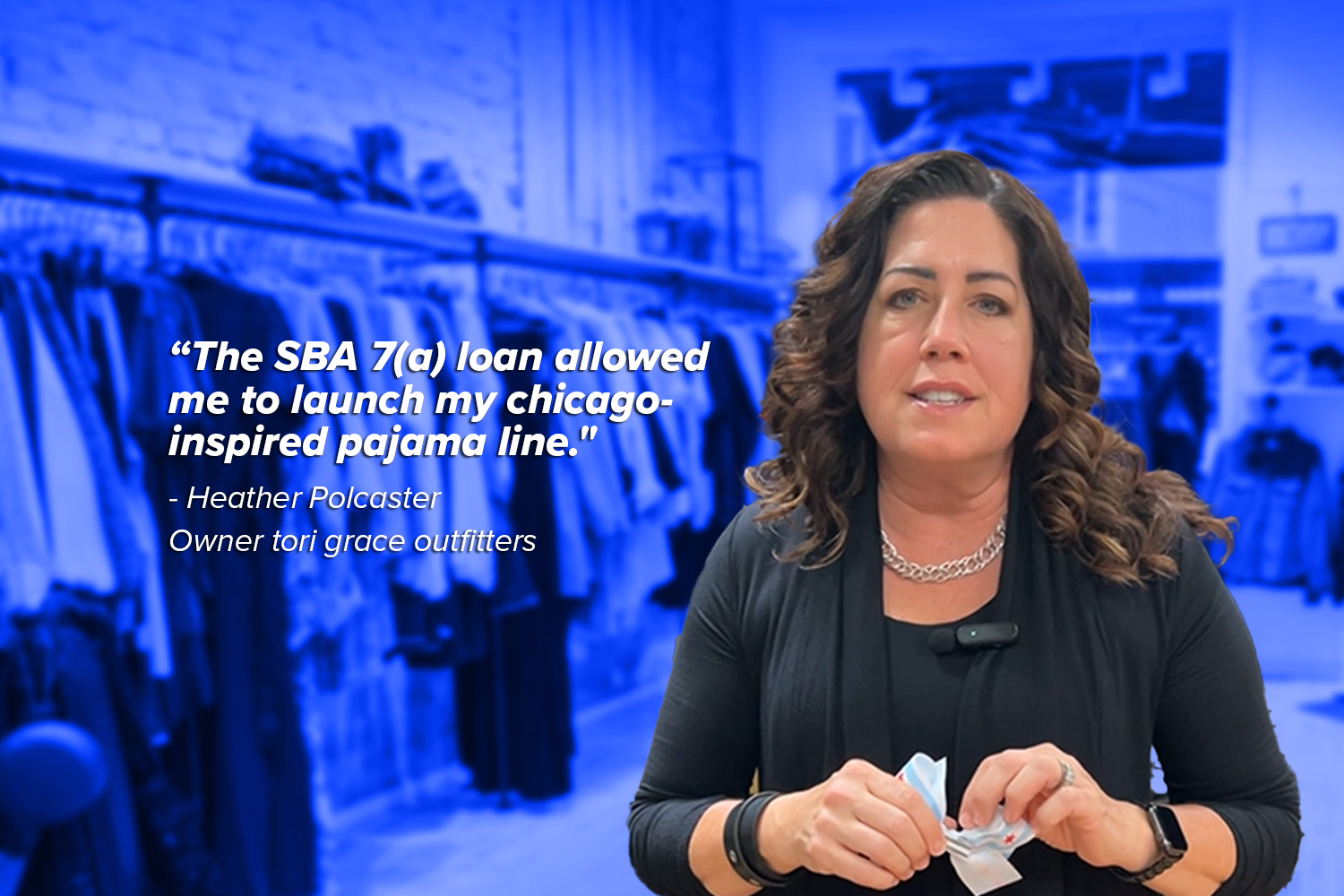

Meet Heather Polcaster – Tori Grace Outfitters

“Most of my years in business I was sewing and making everything in my house.” Heather Polcaster Owner of tori grace outfitters Meet Heather Polcaster,

Grants vs. Loans: Small Business Financing

Securing financing is crucial for the success of emerging small businesses. Small business owners have various funding options, including personal savings, loans, grants, crowdfunding, and

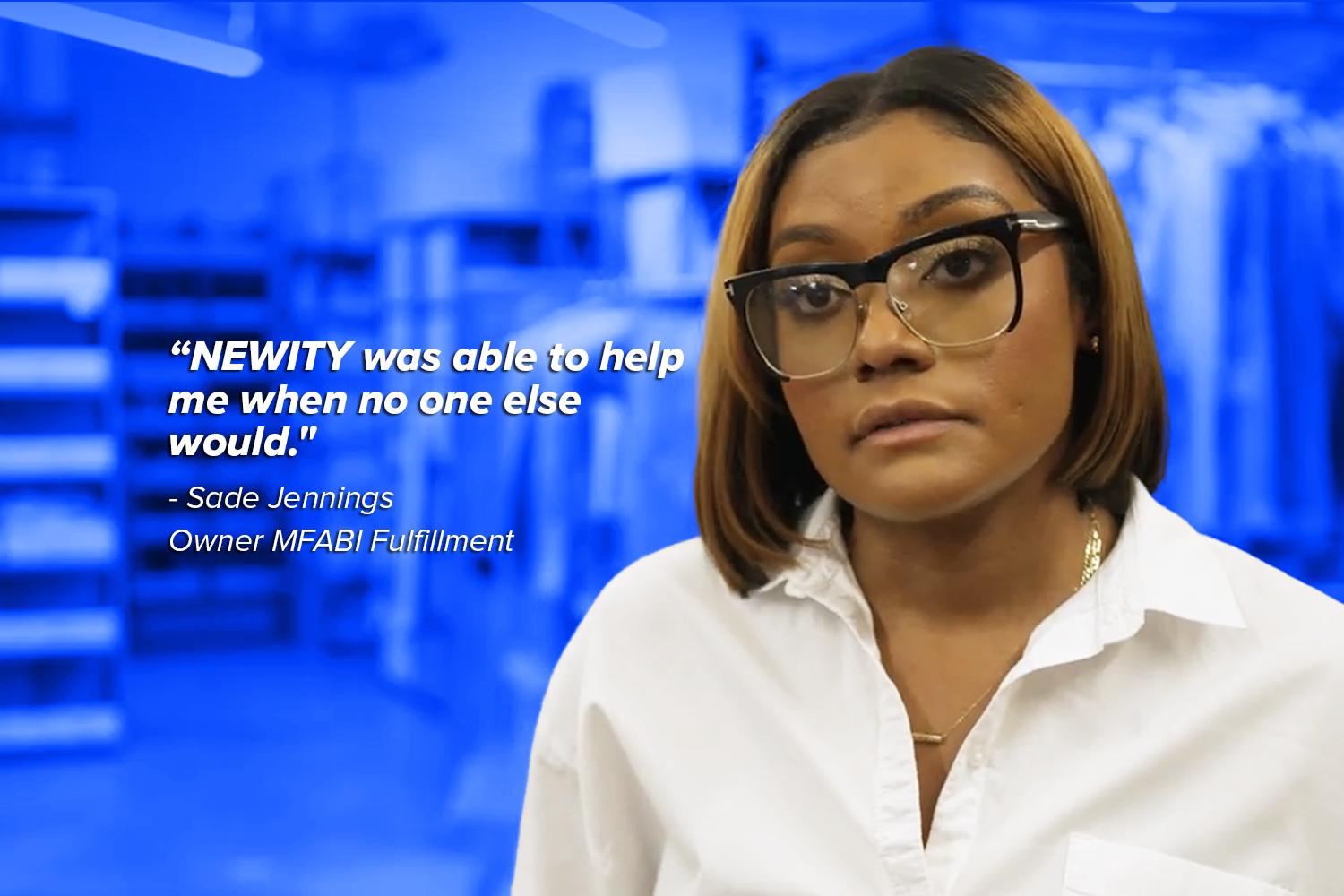

Meet Sade Jennings – MFABI Fulfillment

“What I loved about NEWITY was that they knew the rules and what the SBA needed.” Sade Jennings Owner of MFABI Fulfillment Meet Sade Jenning,

How to get a Larger Business Loan.

When you’re in the process of applying for a small business loan, lenders take a close look at certain metrics to gauge risk. Whether you

Impact of Next Week’s Federal Reserve Meeting on Small Business

Economists predict The Federal Reserve will vote to maintain current interest rates next week, holding off on rate cuts until late 2024 if at all

Top 5 Red Flags to watch for when Applying for a Business Loan

Are you in need of a business loan? Chances are you’ve encountered several loan applications in your search. It’s essential to keep an eye out

Meet Jen Nylin – Jenny in the City

“I encourage you to check out NEWITY, don’t make it hard for yourself, don’t complicate it, let them walk you through the process. It doesn’t

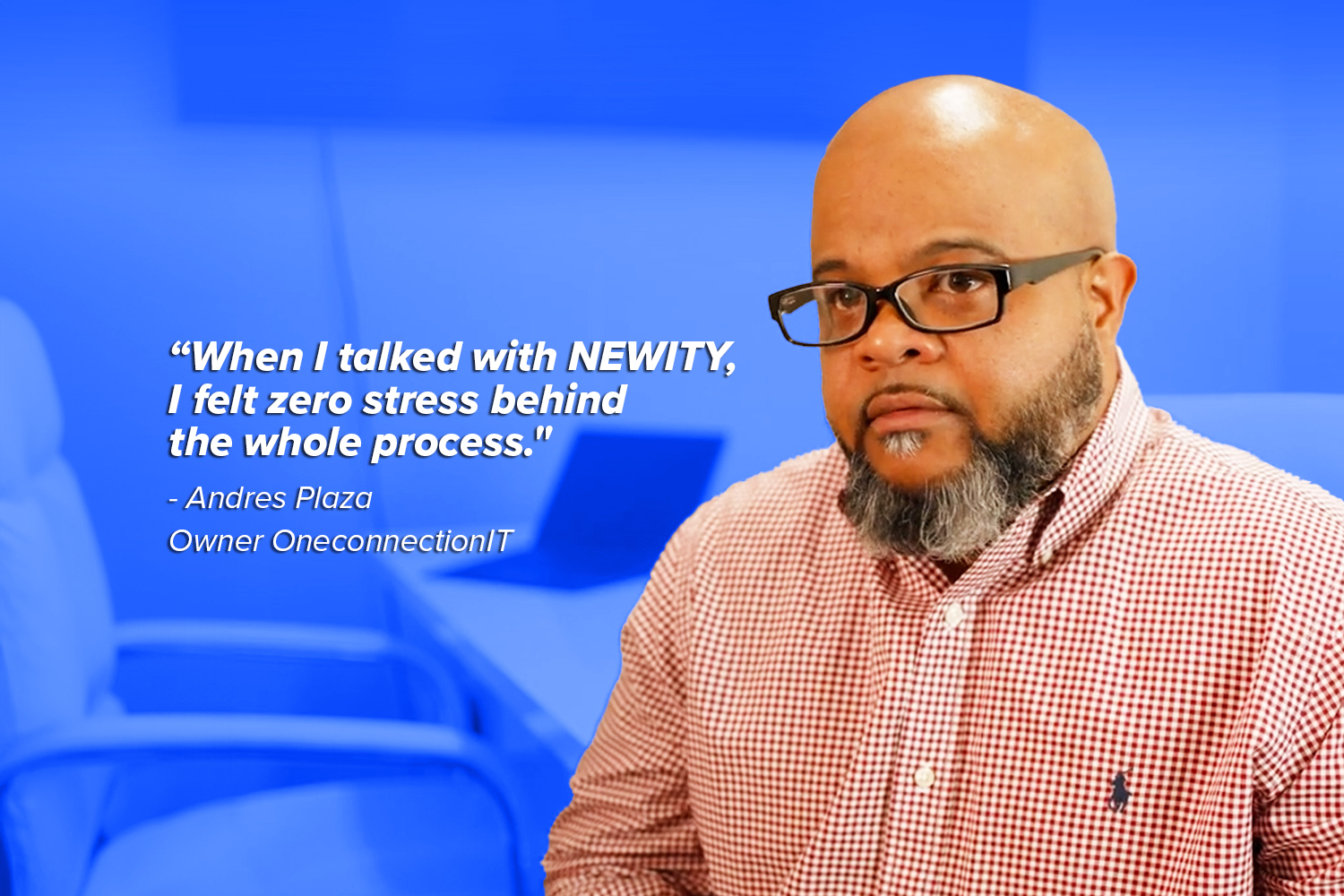

Meet Andres Plaza – OneconnectionIT

“You have to invest to be able to make money and it’s either coming out of pocket or you’re finding someone like NEWITY that’s going

How to Build your Business Credit Score

What is a business credit score? Your business credit score is a number ranging from 300-850 and serves as a measure of your business’ creditworthiness

Are SBA Loan Interest Rates Determined by the Lender?

Key Takeaways Your SBA 7(a) loan interest rate is determined by several factors, including SBA regulations, your lender, and the country’s broader economic state The

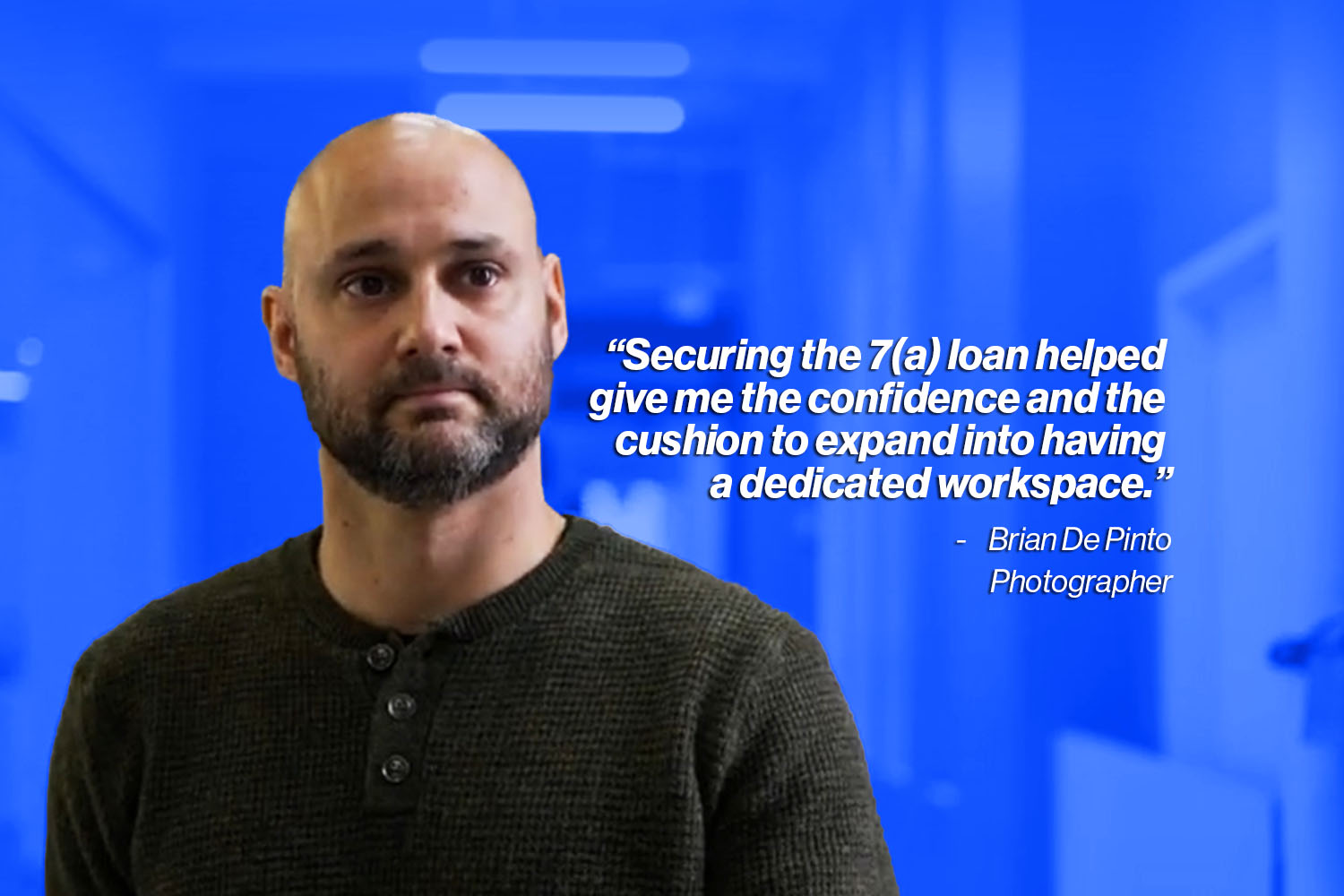

Meet Brian De Pinto – Photographer

“NEWITY really helped demystify the process and helped me get the funding I need to take my business to the next level.” Brian De Pinto

Can I still File for ERC? Has the ERC Filing Deadline Passed?

What you need to know following Tax Day 2024. The Senate continues to debate the bill that could alter ERC program filing deadlines. The existing

How does the WSJ Prime Rate Impact your Business Loan?

Key Takeaways The WSJ Prime Rate is a benchmark interest rate used by banks to set rates on their loan products. In addition to the

How Quickly can you get an SBA Loan up to $350,000?

How quickly can you get an SBA loan up to $350,000? SBA loans along with other government-backed funding are notorious for being slow and time

Top 5 benefits of SBA 7(a) Loans.

How SBA 7(a) loans can help you secure more capital for less. You’ve likely heard SBA loans provide favorable terms compared to other loan options. What are

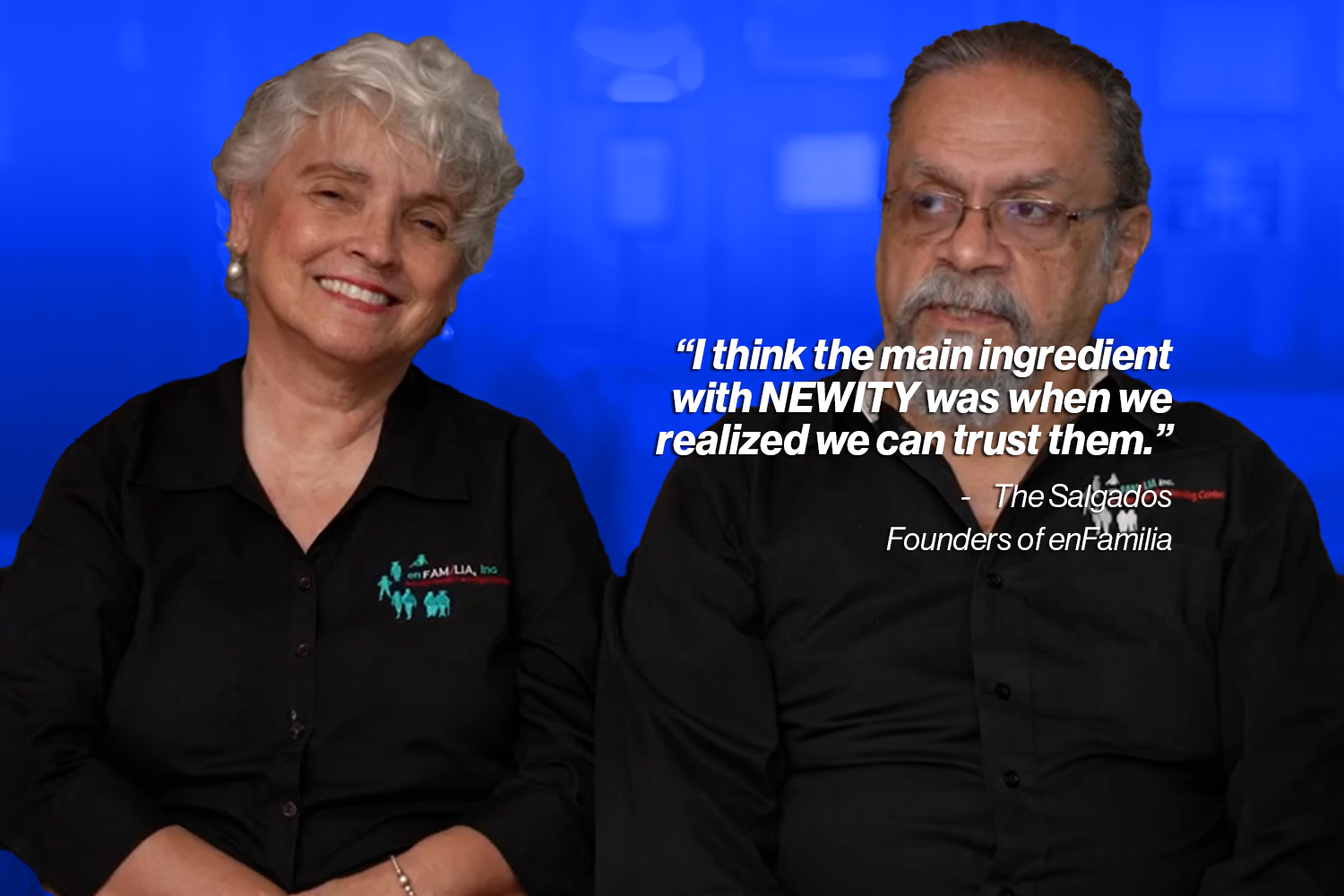

Meet The Salgados – enFamilia

“I think the main ingredient with NEWITY was when we realized we can trust them”. Rocio Tafur-Salgado and Carlos E. Salgado Founders of enFamilia Meet

Small Business Week: How to Prepare

What is Small Business Week? In 1963, U.S. President Kennedy declared the first week of May as National Small Business Week to honor the contributions of entrepreneurs

Legislation Threatens End to ERC

Here’s what small business owners need to know about new legislation that could end the Employee Retention Credit (ERC) program on January 31, 2024. Update

Meet Rachelle Desrosiers – CEO of Madrelle

“I have been with my bank since 2008, and they have never offered the value that I am receiving from NEWITY.” Rachelle Desrosiers CEO of

Is a Grant or Loan Better for your Business?

If grants don’t need to be repaid, are they better than a loan for your business? What’s better, a grant or loan for your business?

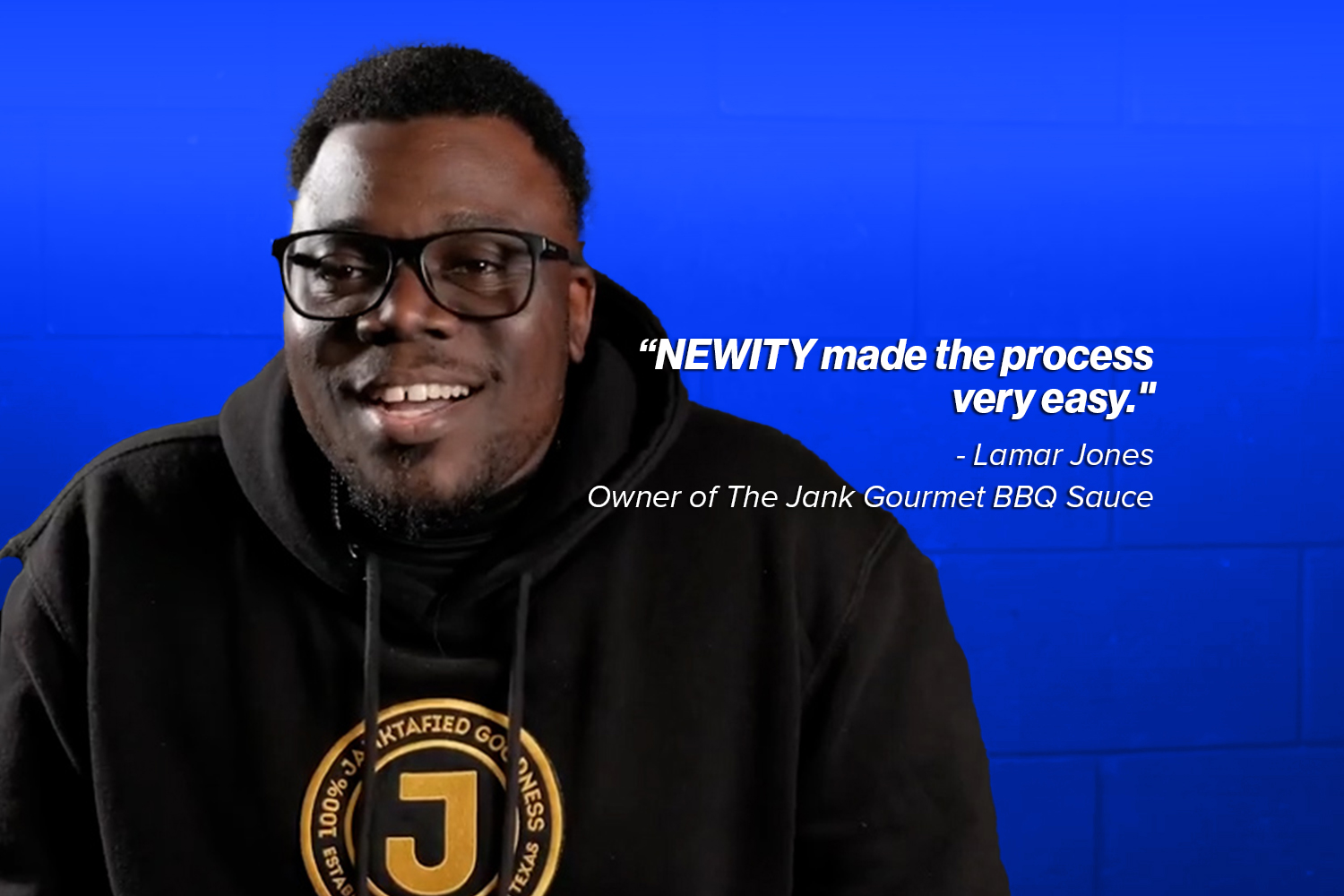

Meet Lamar Jones – The Jank Gourmet BBQ Sauce

“Businesses that exist like NEWITY that are able to help you navigate funding are a big deal.” Lamar Jones Owner of The Jank Gourmet BBQ

How is NEWITY Different?

There are many groups that help small businesses access capital. If you’ve read our article about who provides small business loans, you might have noticed the

Case Study: Securing an SBA 7(a) Loan After Initial Ineligibility.

NEWITY’s approach to helping small businesses secure SBA 7(a) loans, even with low credit scores. GCT Company applied for an SBA 7(a) loan through the

Meet Annessa Pogson – Pack Man Moving

“It’s just one less thing you have to worry about when you’re doing something with NEWITY because you have someone to support you through that

Who Provides Small Business Loans?

A Guide to the Market As the financing market has evolved, new types of loan providers entered the small business loan market. Who are the

A Guide to Small Business Insurance

What is Small Business Insurance? Business insurance refers to a broad category of insurance policies designed to protect businesses against various risks and liabilities. These

Meet Troy Pommier – Kadex Masonry

“We didn’t really have to do much. Provide a few documents here and there and boom it was done.” Troy Pommier Owner of Kadex Masonry

How SBA Loan Rates Compare to Other Options

SBA loans offer some of the lowest interest rates for small business financing. In the table below, we’ve compared the average cost of a $250,000

Is there still time to file for ERC?

A chamber of Congress recently voted to pass legislation that ends the Employee Retention Credit (ERC) program on 1/31/24. Since we’re past 1/31 and into

Don’t Qualify for an SBA 7(a) Loan? – Some Alternative Options

At NEWITY, we aim to help small business owners get access to the capital they need to grow. Obtaining funds for business expansion can be

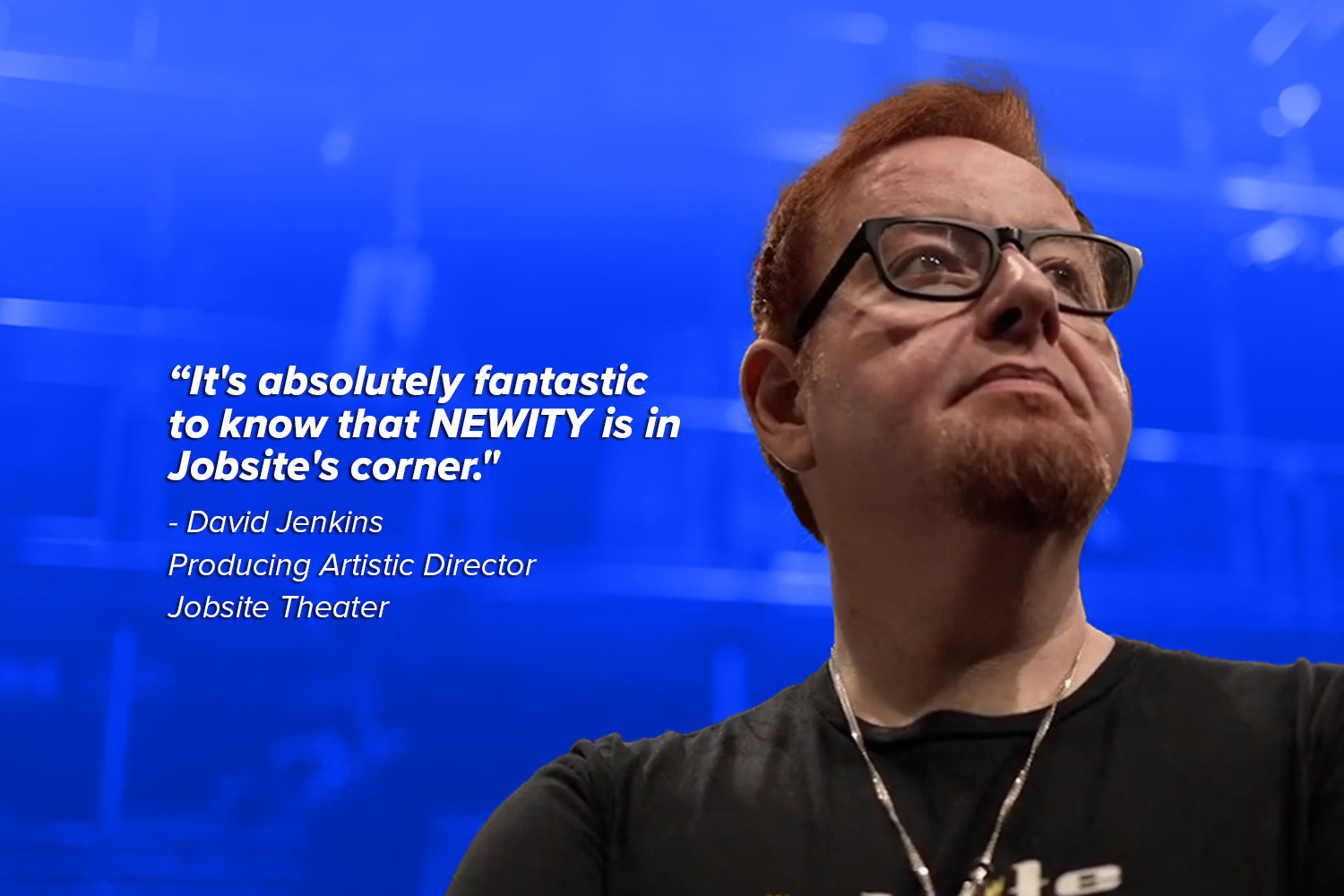

Meet David Jenkins – Jobsite Theater

“What I was most struck by was I had a single human being who helped me from the beginning and was with me every step

Congress Continues to Debate ERC Program

While Congress continues to debate legislation that would effectively end the Employee Retention Credit (ERC) program early – there’s a few things to consider: 1.

Meet Christine and Jonathon Erdeljac – Jonathon’s Diner

“The future is looking really good thanks to partners like NEWITY. It’s nice to know that you have a partner that’s honest, you can work

Meet Frances Hoover – Smith Memorial Playground

“When I am working with NEWITY, I do feel like it’s a company that cares, that I am not a transaction to them, that they

A Letter from our CEOs – What to Expect in 2024

Dear Member, Happy New Year! We’re excited to kick off 2024 with a preview of what lies ahead for our small business offerings here at

Meet Sara McCorriston – Paradigm Gallery

“NEWITY is your support system, they were the team behind you to help navigate what can be a very complicated process. NEWITY is the company

Kickstart your New Year with Cultivate Advisors

As we approach the new year, entrepreneurs and small business owners are gearing up for fresh opportunities, growth, and success. One resource that can play

The Top Seven Business Credit Score FAQs

Credit scores are a key factor in determining your eligibility for a loan. We encounter the following questions from our members most frequently when inquiring

Prepare for tax season with Xendoo, your expert bookkeeping and tax team.

Tax Day will be upon us before you know it! A common mistake many small business owners make is not prioritizing their bookkeeping and tax

How to Maintain and Build Your Business Credit Score

Beyond understanding the factors that contribute to your credit score, there are a variety of scores, ratings, and agencies that can help you build and

Meet Donna Krom – White Mink Hair Salon

“The advice I have for small businesses is hang in there, have faith, and call NEWITY.” Donna Krom White Mink Hair Salon The White Mink

What contributes to your business and personal credit score?

Understanding what contributes to your credit score can help you identify areas in which to improve so you can increase your score. Generally, higher credit

Meet Esosa Edosomwan – The Raw Girl

Esosa Edosomwan, the founder of Raw Girl, is a certified nutrition specialist and behavioral coach. She helps people resolve their health conditions by getting to

Have a COVID-19 EIDL? Three things to know

Did you receive one of the 3.9 million COVID-19 Economic Disaster Recovery Loans (“EIDL”)? If you received a portion of the $380 billion issued through

Top five tips for harvesting year-end success

November and December are pivotal months for many small businesses. Marketing can help you harness the potential year-end earnings. Not sure where to start this

Meet Dr. Thomas Dawes – Dawes Family Medicine

“NEWITY re-ran the numbers and I asked, ‘is this real’? I had a second accountant look it over and they said, ‘Yeah, this is what

Three Ways Thriving Businesses Think About Capital

We often hear from businesses who need capital urgently. Some of the most crafty businesses, however, seek capital without urgency. What are the top three

Meet Matt O’Hara – Brooklyn Dip & Burger

“NEWITY really helped my small business and made me feel important.” Matt O’Hara Founder of Brooklyn Dip & Burger Brooklyn’s Hidden Gem Brooklyn Dip &

SBA 7(a) Eligibility Updates – The New Minimum Requirements for an SBA 7(a) Loan

With the SBA’s latest SOP changes, the minimum criteria required to qualify for an SBA 7(a) loan has lowered for larger loan amounts. To qualify

Four Factors Impacting Your Loan Size

The SBA lowered requirements for larger loan amounts earlier this year. This is great news, but some business owners still don’t understand how lenders calculate loan

How to Receive Your ERC Refund Fast – Even if You Already Filed

With the IRS’ recent Employee Retention Credit (ERC) processing moratorium, many small businesses are seeking solutions to receive their ERC refunds faster. NEWITY provides two

Meet Michael Gurval – ICA Risk Management Consultants

“The thing that sets NEWITY apart is that they take that extra step to go into all of the details. I would highly recommend people

Four Ways to Fuel Your Growth With a Business Loan

How to use a business loan strategically. The SBA recently changed its loan program rules, allowing small businesses to receive larger loan sizes with fewer

The SBA’s New Rules + How It Could Mean More Money for You

On August 1st, 2023, the SBA released Standard Operating Procedures (“SOP”) 50 10 7 with updated rules for approving and funding loans offered through the SBA’s 7(a) program.

Meet Ron Tornari – Chefs for Seniors

“I think NEWITY cares, they understand the small business and they know what we went through. NEWITY made me feel like they were working for

Deciphering the IRS ERC Update – What You Need to Know

On Thursday, September 14, the IRS issued an announcement regarding the Employee Retention Credit (ERC) program. This IRS release contained two major updates. First, a

Meet Dr. Ashok Mehta – SimplyCare

“Who works around the clock to get their customers funding? NEWITY people.” Dr. Ashok Mehta Owner of SimplyCare Patients have trusted this medical practice for

Letter from our CEOs

Hello Member, The IRS recently issued a press release, warning business owners of predatory ERC filers, noting the IRS would be increasingly focused on program

CEO Spotlight – Breef

Breef CEO George Raptis Answers Top 7 Questions For Small Business Owners 1. What is the number one misconception of marketing for small businesses? That

Meet J. Marie Jones – Affirm The Word Literary

“For one thousand times I’m going to say I’m grateful, NEWITY is there as a partner.” J. Marie Jones Owner of Affirm The Word Literary

CEO Spotlight – Xendoo Accounting

Xendoo Accounting CEO Lil Roberts Answers Top 7 Questions For Small Business Owners 1. What is the number one misconception of accounting for small businesses?

ERC Advance Case Study: Beauty Salon

Business Outline Hannah is the business owner of a beauty salon in Seattle, WA. Her business was founded in 2013 and maintained 10-20 employees between

Insurance Requirements for SBA 7(a) Loans

Picture this: You’re moving smoothly down the path of getting funded for an SBA 7(a) loan. Then you discover the SBA requires you have certain types

The Difference Between ERC Fast Track and ERC Advance

NEWITY offers two different ERC programs: ERC Fast Track and ERC Advance. Learn more about each offering and which may be the right fit for you. ERC

Meet Courtland Townsley – Touchstone Group Real Estate

“I wish I ran into NEWITY when I first started business” Courtland Townsley Managing Partner at Touchstone Group Real Estate Going above and beyond expectations

Meet Chelsea Joffray – The Hideout Salon and Lounge

“For any small business, you need funding before you know you need it.” Chelsea Joffray Owner and CEO of The Hideout Salon and Lounge in

Not All ERC Processors Are Created Equal

As we’ve shared, not all ERC processors are created equal. The IRS warns business owners about ERC processors that over-promise credits due to aggressive determinations of

CEO Spotlight – Mylo Insurance

Mylo Insurance CEO David Embry Answers Top 6 Questions For Small Business Owners 1. What is the number one misconception about small business insurance? The

Meet Eric Bryant – Cereal City Pediatrics

“NEWITY came and helped us in our time of need, definitely forever grateful.” Eric Bryant Owner and Pediatrician at Cereal City Pediatrics, Battle Creek, Michigan

SBA 7(a) Loan Prescreen Example: Texas BBQ Restaurant

Business Outline: Javier owns a vibrant restaurant in San Antonio, Texas. He worked hard to retain employees through the pandemic. After the pandemic, San Antonio’s

Meet Kayla Prestel – Feel Good Pilates

“NEWITY saw me and what my business was doing and offered a loan to me when nobody else did, I was invisible to all other

ERC + PPP | Top 5 FAQs you need to know

Did you have a PPP loan? You might qualify for Employee Retention Credits (ERC) because you retained employees during the pandemic. We’ve compiled the top FAQs related

CEO Spotlight – Cultivate Advisors

Cultivate Advisors CEO Casey Clark Answers Top 8 Questions For Small Business Owners 1. What is the number one reason small business owners fail or

Debunking the Top 5 Common SBA 7(a) Loan Myths

SBA 7(a) loans are becoming increasingly popular as credit becomes more difficult to secure from traditional lenders. However, like many government-sponsored products, there’s a significant

Meet Lincoln Baker – LabCo Electric

“NEWITY is filling a void in the marketplace for small businesses like mine, yes, absolutely.” Lincoln Baker Owner of Labco Electric Contracting Corporation in New

Introduction to the SBA’s 7(a) and 504 Program Changes

How 2023 SBA Business Loan Program Changes Will Affect Small Businesses We sat down with NEWITY’s Co-CEOs, Luke LaHaie and David Cody, to hear their

ERC Fast Track Case Study: Law Firm

Business Outline: Alex is the business owner of a law firm in NYC. His business was founded in 1989 and has maintained eight employees over

SBA 7(a) Part III – Frequently Asked Questions During the SBA 7(a) Application

NEWITY is committed to helping small businesses across the United States thrive, which is why we offer SBA 7(a) working capital loans up to $350,000. Compared

How New Businesses Could Claim ERC Up to $100K

New startup businesses that began operations in 2020 or 2021 may be eligible for the Employee Retention Credit (ERC), a significant tax credit worth up to

NEWITY’s Free ERC Shutdown Consultation

NEWITY’s Free ERC Shutdown Consultation: How to Prepare, What to Expect, and What Comes Next We recently sat down with NEWITY’s General Counsel and Executive

Tax Dos and Don’ts for Small Businesses

Most tax years require relatively similar information to the year prior, but business owners in 2023 have the unique opportunity to do more this tax

SBA 7(a) Application and Approval: Construction Management

Business Outline: Jack is the owner of a construction company in New York, NY. As Jack’s company grew, he realized he needed more capital to

ERC Calculation & Refund Example: Coffee Shop Owner

Business Outline Sue is the owner of a coffee shop in Michigan. Her business was founded in 2018 and she maintained 24 employees throughout 2020,

Top ERC Questions Answered By NEWITY’s ERC Expert Dane Colvin

NEWITY sat down with Employee Retention Credit (ERC) expert Dane Colvin, who recently hosted NEWITY’s How To Apply For ERC webinar. Spearheading the ERC program from

SBA 7(a) Loan Application Part 2: Documentation

NEWITY is committed to helping small businesses across the United States thrive, which is why we offer SBA 7(a) working capital loans up to $350,000.

Preparing for the SBA 7(a) Loan Application Part 1: Loan Eligibility

NEWITY continues its commitment to help small businesses thrive by offering SBA 7(a) working capital loans of up to $350,000. SBA 7(a) loans are an attractive

Key PPP Forgiveness Questions for 2023

As the Paycheck Protection Program (PPP) has come to a close and most loan forgiveness decisions have already been made, NEWITY is here to answer

5 Benefits of SBA 7(a) Loans Compared to Alternatives

When searching for capital to grow your business, it can be difficult to discern the differences between financing options and loan types. This article outlines

Three Red Flags to Look Out For in ERC

Not all Employee Retention Credit (ERC) processing companies are equal. Here are three ERC processing red flags that you should never ignore. 1. Your ERC

7-Step Checklist for Year-End Accounting

The end of the year is a stressful time for small business owners, not only because of the holiday season, but also due to year-end

Answering Key Question About Employee Retention Credit (ERC)

NEWITY recently hosted a webinar on the Employee Retention Credit Program with Luke LaHaie, Co-Founder and Co-CEO and Dane Colvin, Senior Associate FP&A. They answered

SWOT Analysis for 2023 Planning

Small businesses are operating in a very different world post-pandemic. While COVID-19 created new obstacles for companies of all sizes, we can apply the lessons

Insurance Group Benefits: Definition, Types, and Costs for Small Businesses

Now that your business is up and running and you may be wondering if you can afford to start offering insurance – also known as

How Much Does a Bookkeeper Cost?

As a small business owner, you likely have a long to-do list and may not have the time or expertise to manage your own bookkeeping.

What are my Options if my PPP Loan is not Forgiven?

The Paycheck Protection Program (PPP) was implemented to provide financial relief to U.S. businesses during the COVID-19 pandemic. According to the latest data from PandemicOversight.gov,

The #1 Way to Boost your Likelihood of Approval for an SBA 7(a) Loan

The 7(a) loan program through the Small Business Administration (SBA) was created to provide access to capital for US small businesses who may otherwise have

What is the Employee Retention Credit (ERC) and Does My Business Qualify?

The pandemic prompted the creation of various programs to support small businesses. While most COVID-19 aid has ended, the Employee Retention Credit (ERC) is still

How to Identify your Target Audience as a Small Business

Marketing a small business comes with many challenges. How can you ensure you are targeting the right people with the right messages?

Since defining a

What Happens in a SBA Review After Applying for PPP Forgiveness?

The Paycheck Protection Program (PPP) was created to provide financial relief to U.S. businesses during the pandemic. If your PPP loan was selected for SBA

Reading your Statement of Cash Flows

Understanding how cash is entering and exiting your accounts is paramount to keeping your business financially healthy. This article will walk you through the specifics

6 Best Practices for Annual Insurance Policy Renewals

When you purchase an insurance policy for your business, the Declarations Page generally outlines the Terms and Conditions of the policy. Once your insurance policy

How Can SBA 7(a) Loans be Used for Small Businesses?

Most U.S. businesses are familiar with the Paycheck Protection Program (PPP) that provided loans during COVID-19, but some may not have heard about 7(a) loans:

PPP Loan Forgiveness: How to Apply and What Happens if I Don’t?

More than 11.5 million Paycheck Protection Program (PPP) loans were issued as financial relief during the COVID-19 pandemic. Loans are forgivable for businesses that used

The Top 3 Small Business Financial Statements You Need

If you are like most small business owners, accounting likely is not the reason you got into business, but understanding your key financial statements can

How to Build a Small Business Content Marketing Strategy

Most small business owners understand that marketing should play a role in their operations, but many don’t know where to start. One of the most

Do Small Businesses Need Cyber Liability Insurance?

As a small business owner, there’s a significant risk that you may not be paying enough attention to: cyberattacks. It’s becoming more common for cybercriminals

The Best Loan Option for Small Business

You’re Looking to Grow Your Business… Where Do You Start? You had a vision that you made a reality. But when it comes to expanding

7 Top Strategies for Small Business Customer Retention

No matter which type of business you own, you have likely contemplated the merits of which is more important: customer retention or customer acquisition. The

Beyond PPP Loans: What’s the Next Option for Small Business Capital?

The Paycheck Protection Program (PPP) was an extremely popular financing option for many U.S. small businesses during the COVID-19 pandemic, as it offered favorable terms,

Small Business Accounting Preparation Before a Possible Recession

Small and medium businesses make up the vast majority of the U.S. economy – 99.9% of all businesses – so it’s understandable why many small

The Importance of Management Liability Insurance During a Recession

Economic downturns and recessions bring about a variety of challenges for businesses, from the obvious risk of lower revenues and higher costs, to less discussed

How SBA 7(a) Loans Help Small Businesses During a Recession

If you’re like most small business owners, you’re probably keeping a close eye on expert predictions about whether a recession is coming (or has already

The 7 Insurance Policies Every Restaurant Needs

When you first decided to open a restaurant, it was likely because of your love of food or a great concept idea. But having the

Social Media Marketing For Small Business Owners

As a small business owner , you know better than anyone that marketing can make or break your business. In 2022, social media marketing is

4 Crucial Metrics Behind Making Better Business Decisions

Business owners are busy and don’t have endless time to spend analyzing their financial data. Despite this fact, it is absolutely worth investing time to

What to Know About Life Insurance for Business Owners

The goal as a business owner with a life insurance policy is to protect your business as well as your family financially, while ensuring that

How To Plan Your Marketing Roadmap

In small business marketing, it pays to have a plan. Business owners can derive the most value from their marketing efforts by tracking key metrics

PPP Simple Forgiveness Journey using Form 3508S

If your PPP loan amount is $150,000 or less, you qualify to file for forgiveness using Form 3508S which is a one-page simplified version of

Using 7(a) Working Capital Financing To Fight Rising Costs Due To Inflation

Inflation in the United States has soared in the past year to 8.5% and according to many experts it is here to stay for the

Financial Templates: Balance Sheet, Profit & Loss, and Personal Financial Statement

One of the most important items on the list of a small business owner is to keep track of their finances. After guiding many small

Quick Guide to Business Insurance: How to Protect Your Business

Owning a business can be exciting and overwhelming. To protect your business and maintain your success, it’s important to have proper business insurance coverage. Not

5 Hidden Costs of Doing Your Own Small Business Bookkeeping

If you’re like many small business owners, doing your own bookkeeping may be a source of pride – especially if you’ve done it from the

A Business Insurance Roadmap

Your company changes over time, follow our roadmap to understand the insurance decisions you need to make along the way.