SBA Loan Basics

Everything you need to know about SBA small business loans

Your guide to SBA loans

SBA loans are government-backed loans for small businesses. They offer lower interest rates, longer terms, and higher approval rates than most traditional loans.

At NEWITY, we make it faster and easier to apply.

What is an SBA loan?

An SBA loan is a small business loan backed by the U.S. Small Business Administration (SBA). The SBA doesn’t lend money directly. Instead, it partners with approved lenders and guarantees a portion of each loan. That guarantee means lenders can offer better terms to more businesses. SBA loans tend to have:

- Lower interest rates than traditional business loans

- Longer repayment terms (up to 10 years)

- Higher approval rates

- No down payment or deposit required (through NEWITY)

SBA Loan Programs Through NEWITY

NEWITY offers access to three SBA loan programs

SBA 7(a) Loans

up to $350,000

This is the SBA’s flagship loan program.

The funds can be used for many business needs like payroll, inventory, debt refinance, working capital, and more.

SBA Made in America Loans

up to $1,000,000

Built for U.S. manufacturers.

Use the funds to buy equipment, build your supply chain, bring jobs back to the United States, or grow your existing domestic team.

SBA Grocery Guarantee Loans

up to $1,000,000

Built for food and agriculture businesses.

Designed to help farms, ranches, food processors, and grocery stores grow and keep food costs low.

Why SBA Loans Beat Traditional Business Loans

SBA loans provide seven primary benefits as compared to traditional business loans:

Lower interest rates — SBA loans carry lower rates than most conventional loans.

SBA loans through NEWITY are priced at WSJ Prime + 2.75% to 3.75%, currently 9.50% to 10.50%*.

Higher approval rates — The SBA’s mission is to help small businesses access capital.

Approval rates are higher than traditional loans with similar terms.

Wide variety of uses — SBA loans can cover a wide range of costs like payroll, rent, inventory, debt refinance, equipment, and more.

SBA loans through NEWITY can be used for everyday expenses, also known as working capital.

Longer terms, lower payments — All SBA loans through NEWITY have 10-year repayment terms.

Longer terms mean lower monthly payments, which frees up cash to run and grow your business.

No relationships required — Traditional bank loans often favor long-term customers.

SBA loans are based on your business financials, not your history with a specific bank.

Simple Documents — Most business already have the required documents.

These can include tax returns, bank statements, and a debt schedule.

Soft credit check to apply — Applying through NEWITY uses a soft credit pull.

Your credit score is not affected when you check if you qualify.

Do You Qualify?

Basic Requirements

To qualify for an SBA loan through NEWITY:

- Your business must be U.S.-based and for profit

- Be in business for at least two years

- Have at least $100,000 in annual revenue

- Meet basic SBA requirements (if you recieved a PPP loan, you likely qualify)

With NEWITY, you can see your loan amount in less than 10 minutes.

Interest Rate & Terms

Interest rates for SBA loans are based on the WSJ Prime Rate plus a lender spread. Through NEWITY:

Rate: WSJ Prime + 2.75% to 3.75%(currently 9.50% to 10.50%)*

Term: 10 years

Prepayment Penalties: None

Down Payment: None

Documents

You don’t need documents to find out if you qualify. Documents are only needed if you qualify and choose to move forward.

- Most recent personal tax return

- Most recent business tax return

- Last 6-12 months of business bank statements (or connect through Plaid)

- Business debt schedule, if applicable

- P&L Statement and Balance Sheet for larger loans

* WSJ Prime Rate is 6.75% as of December 11, 2025. Interest rates vary from WSJ Prime + 2.75% to WSJ Prime + 3.75% based on the business and personal credit scores of the borrower and owners, the amount borrowed, and risk profile of the business.

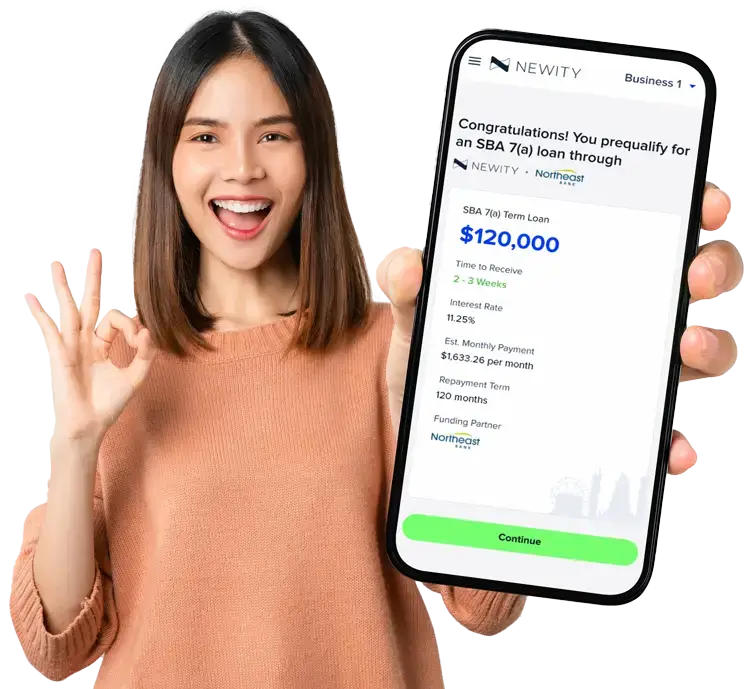

How much can I receive through an SBA 7(a) loan?

Through NEWITY, most businesses can receive an SBA 7(a) loan up to $350,000. Manufacturing and food supply businesses can receive up to $1,000,000.

SBA Loan Calculator

Start your capital journey with NEWITY

Create an account and apply. It takes less than 10 minutes.

Webinars

Learn more about SBA loans.

SBA 7(a) Loans | How to Apply

If you’re looking for $350,000 in SBA funding, this video is for you.

SBA's New Rules for 7(a) Loans

If you want to know more about SBA rules, watch this webinar.

Frequently asked questions about SBA loans

No. NEWITY uses a soft credit check. Seeing if you qualify will not impact your credit score.

Loan amounts are based on your average annual revenue and cash flow. You will need to generate at least $8,334 per month in revenue or at least $100,000 per year in revenue to qualify.

There are three main reasons small businesses don’t qualify:

- The business does not meet SBA requirements.

- The owner or business’s credit score is too low.

- They don’t earn enough revenue.

If you don’t qualify today, you can reapply after 90 days.

No, at NEWITY, there is no down payment or deposit. Plus, there is no fee to determine if you qualify for a loan.

NEWITY offers alternative options if you don’t qualify for an SBA program. We’ll help match you with the best available option for your business.